I Spent $1500 to Get My Real Estate License... and Never Used It.

A four-year, three-school, two-crash-course journey through California's Department of Real Estate... and what the Instagram gurus won't tell you about turning a license into income.

The True Cost Series · #001

If you've spent any time on Instagram or TikTok in the last year, you've seen some version of this ad. A guy in Lululemon shorts. Beach behind him. Voiceover full of confidence.

"I took a 3-month course. Got my real estate license. Helped my friend buy a $2M home in Santa Monica, and made $60,000 in commission on my way to six figures in 2026. 💰

Comment SOLD if you want to do the same."

It's a great pitch. Three months of work. Sixty grand. One transaction.

I know because I bought it. Not the course this guy was selling, but the underlying fantasy. That getting a real estate license was a fast, cheap path to keeping commissions in my own pocket and maybe building a side hustle on the way.

Here's what actually happened.

Part One The reason I wanted a license in the first place

In 2017, I bought my first property, a studio, in Oakland, CA.

Sale price: $352,000.

At the time, real estate commissions were almost universally 6% of the sale price, split between the buyer's and seller's agents. Three percent each.

$352,000 × 6% = $21,120 in commission. And $10,560 of that came out of my pocket as the buyer.

I started doing the math in my head: If I had my license, I could pocket the buyer's side of that commission on my own deals. Maybe I could even help friends buy and sell. An extra revenue stream.

That napkin math is what eventually cost me $1,500 and four years.

Part Two The four-year saga to actually get it

July 2019

Bought Real Estate Express. Hated it.

Paid $314.30 for the "Ultimate Learning" bundle. It was all books and reading. I'm an Enneagram Type 7. I learn best from live instruction and pre-recorded videos, not from sitting alone with a textbook. I extended my access. Then I let it expire anyway.

March 2022

Sabbatical. Tried again with CA Realty Training.

$529.98 for live webinars + video. Saturdays, 10 AM to 2 PM, for three months. This format actually worked. I finished the coursework at the end of June 2022.

June 2022 to Jan 2023

Did not sign up to take the test.

Traveled. Went to weddings. Tried other side hustles. The license sat in limbo while I lived my life.

Jan to Feb 2023

Crammed. Bought two more crash courses.

$100 for a CA Realty Training crash course. $69 for a PrepAgent crash course two days before the exam. Skipped a Super Bowl party to study. Studied 5 to 6 hours a day for a solid month.

Feb 2023

Passed the exam on the first try.

License issued by the California Department of Real Estate. I'm officially a licensed real estate salesperson in the State of California.

And then I never used it. Not once.

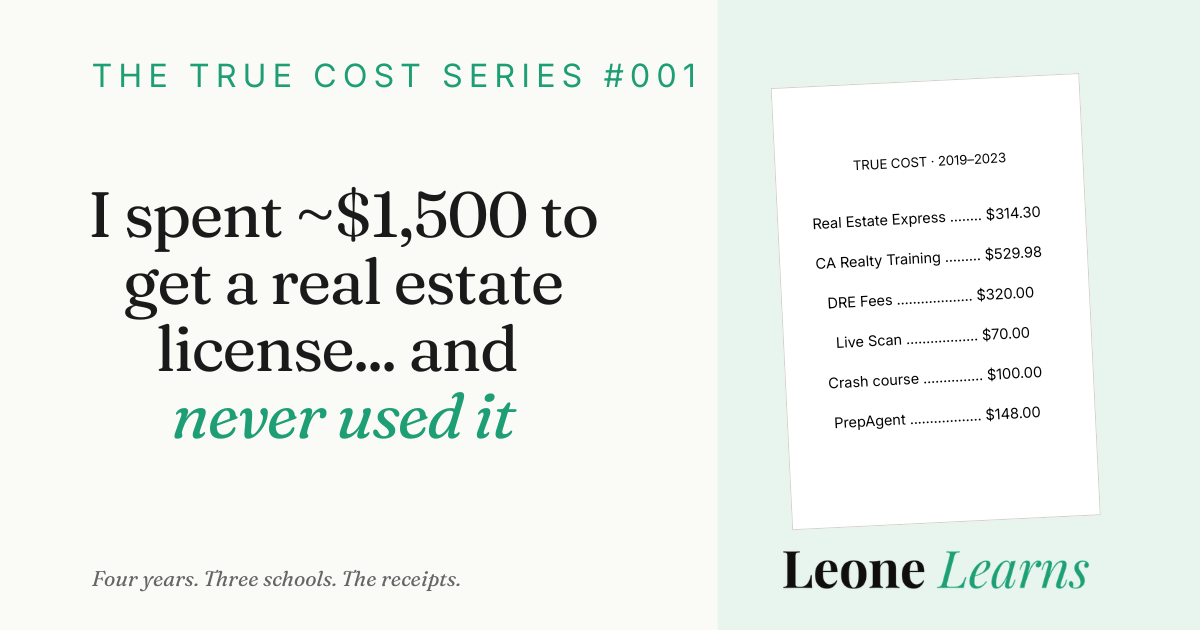

Part Three The receipts. All of them.

Here's every dollar I actually spent. I have the email receipts to prove it.

Line item

Amount

Real Estate Express | Ultimate Learning bundle (abandoned)

Jul 24, 2019

$314.30

CA Realty Training | Live + Online + Video bundle

Mar 17, 2022

$529.98

DRE Exam Fee + License Fee

2022

$305.00

Live Scan / Fingerprinting

2022

~$70.00

CA Realty Training | Crash Course + Exam Prep

Jan 26, 2023

$100.00

PrepAgent | California Exam Crash Course

Feb 10, 2023

$69.00

PrepAgent | 1 month subscription

Feb 2023

$79.00

DRE Exam Scheduling Fee

Feb 7, 2023

$15.00

Total spent

$1,482.28

And that's before hanging the license with a brokerage. More on that in Part 2 of this series.

Part Four The actual time it takes

The fantasy says "3 months." Here's the real time accounting, broken into the two parts that matter:

The classes

California's Department of Real Estate requires 135 hours of pre-licensing education, three 45-hour courses (Real Estate Principles, Real Estate Practice, and one elective). DRE rules also cap you at 2 courses per 5 weeks, and a single course can't be done in less than 2.5 weeks.

So the absolute fastest you can finish the classes is about 7.5 weeks. Most people spread it across 3 months.

For me, that meant about 6 hours a week of class time for 12 weeks, manageable while doing other things.

The studying

This is where the fantasy ads lie hardest. Taking the classes ≠ being ready for the exam.

I studied 5–6 hours a day for roughly a month before sitting for the test. That's another 150+ hours on top of the class hours.

Realistic time investment: ~75 hours of classes + ~150 hours of studying = ~225 hours of focused work. Spread across 4 dedicated months.

A hack worth knowing

If you're a licensed California attorney, you're completely exempt from the 135-hour pre-licensing education requirement. You can register straight for the exam. Same for anyone who's already completed the 8 statutory courses required for a broker's license.

If you have older college credits in subjects like Real Estate Principles, Business Law, or Escrow, the DRE may accept official transcripts in lieu of taking the classes. (I had some old coursework that probably qualified, but my transcripts were from too long ago and I didn't bother. Worth checking if yours are recent.)

Part Five So why didn't I ever hang the license?

Three reasons. None of them were "the fantasy ad lied," though, spoiler, it did.

1. Life happened.

I passed the exam in February 2023. My grandma died in April 2023. I pivoted hard into job-hunting and had an offer by the end of June. Thus, the license stopped being a priority.

2. I asked a friend's dad (a broker) to hang it. He said no.

He didn't want to take on the liability of a non-active agent on his roster. Fair enough.

I wasn't trying to grind out cold-calling weekends and open houses. I wanted an apprenticeship-style arrangement, show up when I had time, be helpful, learn the business. That's not how most brokerages work.

3. The math stopped making sense.

Between fingerprinting, classes, exam fees, and study materials, I'd already spent about $1,500. To actually start working, I'd then need to:

- Pay desk fees to my brokerage (often $50–$200/month)

- Pay MLS fees and association dues (a few hundred per year)

- Split 50% or more of every commission with the broker until I hit a cap

- Pay for E&O insurance, signage, marketing, and continuing education

And that's all before I sold a single house. Without an established sphere of influence, meaning a network of friends, family, and contacts actively buying and selling, those costs come out of my savings.

Part Six The NAR change made the side-hustle math worse

In August 2024, as part of a $418 million class-action settlement, the National Association of Realtors changed how buyer's agents get paid. Sellers can no longer offer guaranteed commissions to buyer's agents through the MLS. Buyers now negotiate compensation directly with their agents, and increasingly, sellers are countering with much lower buyer-agent fees, or none at all.

I'm watching this play out in real time on my own deal.

I recently put in an offer on a Mid-City fourplex listed at $1,499,000. My buyer's agent (a luxury agent friend of mine, more on her in a second) requested 2.5% to the buy side in our offer: $34,625.

The seller's counter? 1.75% ($25,812.50). Almost $9,000 lopped off the buy-side commission, just like that.

That's one deal. Multiply that haircut across every transaction in 2026, and the side-hustle math gets ugly fast...especially when you're already splitting whatever you do earn 50/50 with your broker.

Part Seven The other reason I haven't hung my license

Even if the commission math worked, there's a quieter reason I'm glad I never tried to represent myself.

I don't actually know what I'm doing.

That same Mid-City fourplex? It wasn't a clean deal. Here's what I was actually walking into:

- Bank-owned foreclosure. Different paperwork, different timelines, "as-is" terms, and an institutional seller that doesn't negotiate like a person.

- A non-paying tenant in place. Eviction risk, cash-for-keys negotiations, California tenant protections, and a ticking clock on lost rent.

- Multiple open permits. Unfinished work that could mean code violations, surprise remediation costs, or title issues at close.

If I'd been representing myself on that deal, I would have been negotiating against a seasoned bank's REO team, evaluating tenant law I don't know, and decoding permit history I'd never seen, all while trying to close on a $1.5M asset.

Instead, I had my friend, a luxury agent with 18+ years of experience, who's owned multiple investment properties herself, and who has reversed a Wells Fargo foreclosure for a previous client.

She's been a godsend. I would have made expensive mistakes without her.

For the record, that fourplex deal didn't work out for me anyway. The seller would only come down $25K from list. I needed to be $100K below to make the numbers work for me. So I walked. As of this writing, the deal is pending with another buyer.

But the lesson from those two months of negotiation is exactly the one the Instagram ads will never tell you:

The 3% you "save" by being your own agent is meaningless if you don't know what you're doing. One missed disclosure, one mishandled tenant negotiation, one undiscovered open permit... and you've lost ten times what you saved on commission.

Part Eight So... should you get your license?

Honest answer: it depends. Here's how I'd think about it.

Probably worth it

- You have flexible work hours or part-time freedom

- You actively enjoy real estate as a category

- Your existing network is buying or selling regularly

- You're part of an investing group doing BRRRR or flips

- You're willing to network and educate publicly

Probably not worth it

- You only want to save commission on your own home(s)

- Your job has zero flexibility for showings

- You don't enjoy selling yourself or networking

- You don't have anyone in your sphere actively transacting

- You expect a steady paycheck (this is 100% commission)

Part Nine Do I regret it?

No. Genuinely no.

I learned a ton about the mechanics of real estate transactions, contract law, fiduciary duty, and how brokers actually make money. That knowledge has made me a sharper buyer and a sharper investor.

What I do wish is that someone had walked me through the true cost, in dollars and in time and in personality fit, before I started.

That's why this post exists. That's why Leone Learns exists.

I'd rather spend an hour reading someone's honest receipts than three months chasing someone's Instagram fantasy.

My license expires in February 2027. I'm actually leaning toward renewing it and trying to hang it part-time with a niche brokerage I admire, one that focuses on TICs and rentals, just to learn the ropes from the inside.

If I do, you'll get the receipts on that, too.

Up next in this series

How much it actually costs to hang your license.

Desk fees, MLS dues, broker splits, E&O insurance, the stuff nobody puts in the Instagram ads. Subscribe and I'll send Part Two the day it goes live.

Subscribe to Leone Learns →

Subscribe to my newsletter

Join readers getting real numbers from real experiments. Free, no spam.

Member discussion